QuantEvolve: How LLM Multi-Agents 'Evolve' Quant Strategies

The quant version of AlphaEvolve. A paper review of QuantEvolve — a framework that auto-generates and evolves trading strategies using LLM multi-agents + evolutionary algorithms.

If AlphaEvolve solved math problems, QuantEvolve evolves trading strategies. Presented as an oral paper at ACM ICAIF 2025, this paper proposes a framework that automatically generates quant strategies using LLM multi-agents + evolutionary algorithms.

The Problem: Why Existing Approaches Fall Short

Existing LLM-based quant systems (AlphaGPT, R&D-Agent-Quant, etc.) focus on alpha factor discovery. They're good at finding individual signals, but can't build complete strategies (end-to-end) that include position sizing, risk management, and execution logic. Plus, chasing a single "optimal strategy" makes you vulnerable to market regime changes.

Core Ideas of QuantEvolve

1. Quality-Diversity Evolution: Feature Map

Figure 1: QuantEvolve Framework Architecture

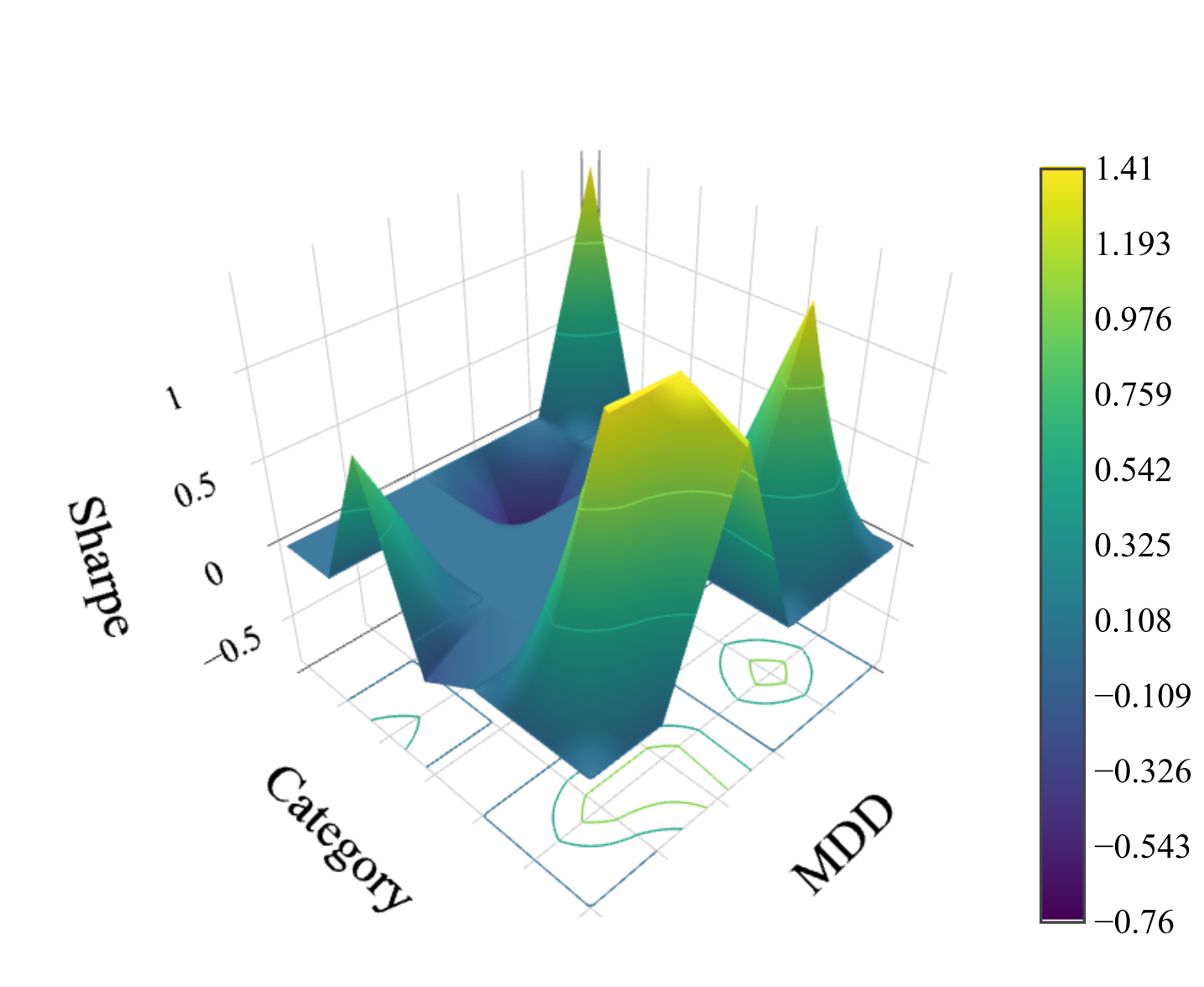

Instead of optimizing strategies with a single objective function, QuantEvolve places them on a Feature Map — a multi-dimensional grid. Each dimension maps to investor preferences:

- Strategy Category (momentum, mean reversion, arbitrage, etc. — binary encoding)

- Sharpe Ratio (risk-adjusted returns)

- Maximum Drawdown (MDD)

- Trading Frequency

- Cumulative Returns

Each cell stores only the single best strategy for that combination of characteristics. This lets diverse risk-return profiles coexist and prevents mode collapse.

2. Island Model: Balancing Exploration and Convergence

Figure 3: Strategy Exchange Between Islands

Multiple "islands" evolve strategies independently, periodically migrating the top 10% to neighboring islands. Early on, each island deep-dives into specialized strategies (momentum, mean reversion, etc.). Later, cross-pollination produces hybrid strategies.

3. Hypothesis-Driven Multi-Agent System

Figure 2: Multi-Agent Evolution Architecture

Strategy generation runs through a 3-stage agent pipeline:

- Research Agent — Analyzes parent + cousin strategies → generates new hypotheses (grounded in finance theory)

- Coding Team — Implements hypotheses in Python → Zipline backtest → iterative debugging

- Evaluation Team — Analyzes hypothesis, code, and results → extracts insights → passes to future generations

The key is insight accumulation. Failed approaches (30+) are documented with why they failed, preventing the same mistakes. Far more efficient than pure random mutation.

4. Parent-Cousin Sampling

When creating new strategies, the system selects 1 parent + 7 cousins from the Feature Map:

- Best Cousins (2): high-performance strategies

- Diverse Cousins (3): strategies adjacent to the parent in Feature Space

- Random Cousins (2): random selection

This structure achieves exploitation (inheriting high performance) and exploration (discovering new combinations) simultaneously.

Results

Equities (AAPL, MSFT, AMZN, GOOGL, META, NVDA)

The evolution process is impressive:

Figure 7: Evolution of Optimal Strategy in Equity Markets

- Gen 0: Volume-momentum signal (simple)

- Gen 10: Multi-timeframe momentum + volatility filtering → returns↑ drawdown↑

- Gen 40: Portfolio-level volatility monitoring introduced → drawdown↓

- Gen 80: Cointegration pair trading attempt → failed (cointegration unstable during volatile periods)

- Gen 130: Selective integration of past successes → momentum entry + volatility scaling + trailing stop

The final strategy outperforms all baselines: MarketCap, Equal Weight, Risk Parity, RSI, and MACD.

Futures (ES, NQ)

Figure 9: Strategy Evolution in Futures Markets

- Gen 0: Fixed Bollinger Band mean reversion → SR -1.21 (disaster)

- Gen 10: Adaptive Z-score + momentum confirmation → MDD improved to -15%

- Gen 20: Dual-mode regime detection — low volatility → mean reversion, high volatility → momentum following

- SR 1.03 | CR 37.4% | MDD -15.4%

- Beats both ES (SR 0.66) and NQ (SR 0.97) buy-and-hold

Interestingly, generations after Gen 20 built more complex systems, but generalization performance actually declined. A textbook case of simplicity beating sophistication — the classic bias-variance tradeoff.

Feature Map Evolution

Figure 5: Feature Map Evolution by Generation (MDD × Category dimension, Sharpe Ratio)

The nearly empty Feature Map at Gen 0 gradually fills through Gen 150, with each cell's performance steadily improving.

Insight Evolution

Figure 8: Insight Evolution in Equity Markets

The real value of this framework may lie not in the strategies themselves but in the accumulated insights:

- "Simple volatility indicators fail during crises" → need VIX + moving average combination

- "Volatility thresholds should be calculated per-asset, not portfolio-wide"

- "Regime detection failures stem from volatility annualization errors (the logic itself is valid)"

- 30+ failed approaches documented → future generations avoid the same traps

Tech Stack

- LLM: Qwen3-30B-A3B (fast responses) + Qwen3-Next-80B-A3B (deep analysis) ensemble

- Backtesting: Zipline Reloaded + QuantStats

- Evolution Score: Score = Sharpe Ratio + Information Ratio + MDD (equal weight)

Limitations and Open Questions

- Small data universe — only 6 stocks and 2 futures. Scaling to hundreds of instruments is the real challenge

- Overfitting risk — the paper itself reports performance degradation when complexity increases after Gen 20

- No execution costs — Zipline simulations don't capture real slippage and market impact

- LLM costs — 150 generations × multi-agent = significant API costs (exact figures not disclosed)

Takeaways

QuantEvolve is one of the most concrete implementations of the vision "AI invents trading strategies." Key insights:

- Paradigm shift: from pursuing a single optimal strategy → maintaining a diverse strategy pool

- Value of failure documentation — 30+ failed approaches dramatically improve future search efficiency

- Simplicity wins — moderately complex mid-generation strategies generalize better than complex late-generation ones

A must-read for anyone looking to leverage LLMs in quantitative trading.

Paper: QuantEvolve: Automating Quantitative Strategy Discovery through Multi-Agent Evolutionary Framework

Authors: Junhyeog Yun, Hyoun Jun Lee, Insu Jeon

Presented at: ACM ICAIF 2025 (AI4F Workshop, Oral Presentation)